Disclaimer

This article is for informational and educational purposes only and does not constitute financial advice. The author may hold positions in the assets discussed. Any discussion on jurisdiction, exchanges or custody providers reflect the author's personal views and experiences and is not a personal recommendation. Always do your own research and seek professional guidance before making investment or custody decisions.

Last Updated on July 27, 2025

Key Takeaways

- To stop the hyperinflation, Germany launched the Rentenmark. It circulated alongside the worthless Papiermark and was backed by mortgages on real estate and industrial assets—not gold—which instilled public confidence despite its non‑convertibility.

- The Papiermark was converted at the rate of 1 Rentenmark = 1 trillion Papiermarks. Simultaneously, the Rentenmark was pegged to the US dollar at RM 4.20 = USD 1, roughly restoring the pre‑war gold‑mark parity and stabilising prices within weeks.

- Within days of the new exchange rate, inflation collapsed. Though initially painful, stabilisation allowed government fiscal discipline, debt renegotiation via the Dawes Plan, and the transition to the gold‑backed Reichsmark in 1924 as Germany rebuilt its economy.

- The Rentenmark’s success helped postpone the collapse of Weimar democracy.

The story of the Weimar hyperinflation is a familiar one. But do you know what the rentenmark was and how it worked?

It should be one of the most famous stories in the history of fiat currency. But sadly, barely anyone properly understands it.

Read this article and you will have a better understanding than 99% of the population about how to recover from hyperinflation.

Let’s wind things back to 1914 and the outbreak of the Great War.

Germany, like the other European powers, suspended the gold standard at the outbreak of World War One in 1914, abandoning the goldmark for the papiermark.

By losing the war she suffered a greater financial strain than the Allies and also had the additional post war burden of reparations.

Inflation, which had begun in 1914, got worse as the German government cranked the printing press and created enormous amounts of papiermarks, eventually triggering hyperinflation.

Most people know the inflation stopped when the government stopped printing and introduced the rentenmark, a currency with limited circulation backed by mortgages over German real estate.

But it is less well understood exactly how the rentenmark worked, how it stopped the hyperinflation and how Germany was able to get back on her feet in 1924.

It is a fascinating story, with massive implications for the present day.

I don’t think we are going to go down quite the same path as Weimar Germany did with our current global currency crisis.

But it is worth analysing what the effects of hyperinflation are and how a country might stabilise herself.

Why Was The Rentenmark Introduced?

The Rentenmark was introduced as a temporary measure to try and resolve the currency crisis that Germany found herself in. The hope was that by stabilising the currency it would give the government some breathing room to get the economy and the country back on track and find a long term monetary solution.

Towards the end of 1923 the government of Germany was trying to resolve the currency crisis.

But there were two significant obstacles to currency reform:

- The President of the Reichsbank, Rudolf von Havenstein.

- The dwindling gold supply.

Von Havenstein had presided over the disastrous hyperinflation. He was responsible for the money printing and the destruction of the German currency. Yet his position was for life and he could not be dismissed. He stubbornly refused to step down and was an impediment to reform.

Germany had almost $1 billion in gold before the war. By 1923 this had dwindled to $150 million. Furthermore, that gold was under Von Havestein’s control in the Reichsbank and not able to be utilised by reformers.

The currency reform would have to bring stability without gold.

A number of ideas were floating around in the latter half of 1923. Adam Fergusson, in his famous book on the Weimar hyperinflation, When Money Dies, describes the atmosphere:

“Every kind of plan for currency reform was in the air, based on gold, or rye, or foreign exchange or ‘material values’.”

Who Created The Rentenmark

One of the many ideas for a new currency was the rentenmark, the brainchild of Dr Hans Luther, the Minister of Finance, and Dr Hjalmar Schacht, a banker who would later be appointed by Luther as the Currency Commissioner.

Luther provided the political support while Schacht was the person who administered the introduction of the rentenmark.

What Was The Rentenmark Backed By?

Rather than being backed by gold, the rentenmark would be backed by land and industry.

Fergusson describes how it would work:

“The Rentenbank’s notes were guaranteed in equal amounts by mortgages on landed property and by bonds on German industry — trade, commerce, banking and transport — to a combined amount of 3,200 million gold marks, about £160 million. The maximum note issue in Rentenmarks was to be 2,400 million. The Rentenbank was independent (as the Reichsbank had been) of government interference. In return for special credits of 1,200 million to the Reich — including 300 million Rentenmarks at nil per cent to pay off the floating debt — the government guaranteed not to discount any more Treasury bills with the Reichsbank…It was not legal tender but, rather, ‘a legal means of payment’. It was not convertible into gold, still less into the agricultural or industrial assets which were supposed to back it, although 500 Rentenmarks could be converted into a bond with a nominal value of 500 gold marks. The legal tender was still the mark, dead but mummified, and negotiable because its constancy at a million-millionth of its nominal value was guaranteed in people’s minds by the Rentenmark, itself only another piece of paper with a promise on it.”

Schacht was initially skeptical of the idea, as he would have preferred a gold backed currency.

But he ultimately accepted that Germany did not have enough gold and no foreigner was likely to lend to them in the state they were in.

He would have to attempt to make the Rentenmark work.

In Lords of Finance: The Bankers who Broke the World, Liaquat Ahamed explains:

“From the very first, he had scoffed at the idea of a land-based currency as a pure confidence trick; currencies had to be backed by a highly liquid, easily transferable, internationally acceptable asset, such as gold. He found it hard to believe that someone being paid in the new currency would derive any comfort from the theoretical promise that those currency notes were ultimately convertible into some slab of inaccessible Thuringian woodland or Bavarian pasture or perhaps of a Communist-riddled Saar factory. During the debate on the various currency reform plans, Schacht had forthrightly argued for gold as the foundation for a new currency. While no one could challenge the theoretical basis of his logic, the fatal difficulty had been that Germany simply did not have enough gold for the job.”

When Was The Rentenmark Introduced?

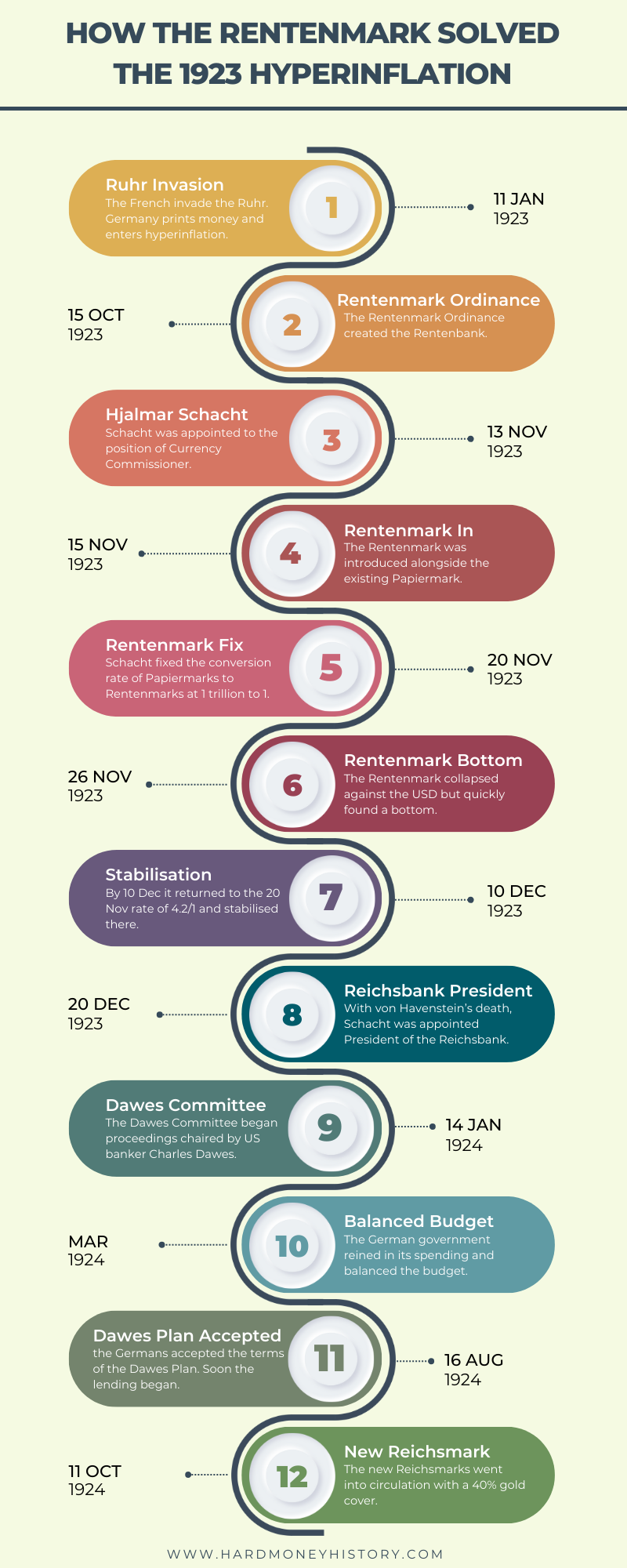

On October 15 1923 the Rentenmark Ordinance was published, which created the Rentenbank.

Fergusson describes it being seen at the time as “radically unsound.” Nobody thought the rentenmark would help.

“Few families can afford meat more than once a week, eggs are unprocurable, milk terribly scarce and bread already sixteen times the price of a few days ago when the maximum price was abolished. It is no doubt true that the expensive restaurants are full of well-dressed people drinking wine and eating of the best in Munich — but they are either German-Americans mistaken for locals, or Ruhr industrialists … No one expects political disturbances, but hunger riots are another matter … and the cold: no one can afford central heating. No one imagines the Rentenmark will help.”

It wasn’t that there was no food being produced in Germany.

The problem was that farmers hoarded their produce and refused to sell it for paper, so people starved in the cities.

In order to alleviate the crisis, Germany needed a stable currency which would be accepted by the agricultural sector.

Luther planned to push ahead and implement the rentenmark.

On November 13 1923 Schacht was appointed by Luther to the position of Currency Commissioner. The Currency Commission was created as an independent body to get around the inconvenience of Von Havenstein in the Reichsbank. His office was a former broom closet in the finance ministry.

Two days later on November 15, the rentenmark was introduced alongside the existing papiermark.

Ahamed describes the situation:

“Germany found itself in the curious position of having two official currencies—the old [papier]mark and the new Rentenmark—circulating side by side, issued by two uniquely parallel central banks. At one end of town was Schacht, operating from his converted broom closet; at the other, Von Havenstein, holed up and increasingly isolated and irrelevant in the Reichsbank’s imposing red sandstone building on Jagerstrasse.”

The Rentenmark to USD

Schacht had to make two early and critical decisions to make:

- The rate to make the rentenmark convertible to the US Dollar, and thus gold.

- The rate to make the old papiermark convertible into rentenmarks.

Over the next several days the papiermark continued to plunge in value.

Fergusson explains the initial impact of the rentenmark.

“The engine of inflation had been put out of gear, but still the country’s finances hurtled downhill under their own stupendous momentum.”

Schacht waited patiently.

On November 20 the papiermark fell to 4.2 trillion to 1 US Dollar. At that point Schacht fixed the conversion rate of papiermarks to rentenmarks at 1 trillion to 1.

The ratio of papiermarks to the pre war goldmark was also 1 trillion to 1, which meant that 1 rentenmark equaled 1 goldmark.

This also set the US Dollar/rentenmark rate at 4.2 to 1.

Over the next few days both the papiermark and the rentenmark continued to fall against the US Dollar. From 4.2 trillion to 1 USD on November 20, the papiermark fell to 11 trillion to 1 by 26 November.

However, by December 10, it had returned to 4.2 trillion to 1 and prices began to stabilise.

The papiermark/rentenmark ratio of 1 trillion to 1 was considered a masterstroke because it made conversion very easy. All a German citizen had to go was remove 12 zeros.

How Did The Rentenmark Bring Stability?

The rentenmark was intended as a temporary currency to bring about stability so that a more permanent solution could be found.

Was the rentenmark successful?

Yes it was. It was a confidence trick but people bought it. Even though the backing of the rentenmark was ficticious, there was enough perceived stability to halt the currency crisis.

Initially the shock of stabilisation brought hardship but eventually life improved.

Ahamed describes the effects:

“When prices were so insanely rising, the average German had done everything he could to get rid of any cash he received as fast as possible. Now this spiral reversed itself. As prices began to hold and then fall, it became profitable to hang on to cash. Farmers, their confidence in money restored, began bringing produce to market, food reappeared in the shops, and those interminable queues began to melt away.”

It wasn’t just monetary policy that solved the crisis. The government reined in its spending and balanced the budget by March of 1924.

And it just so happened that on November 20, the day that Schacht fixed the rentenmark exchange rate, Von Havenstein died of a heart attack.

Exactly one month later, Schacht was appointed President of the Reichsbank. With the rentenmark having the desired effect and in a new job, he was now in a position to start planning long term currency solution.

How Did The Rentenmark Stop Hyperinflation?

The rentenmark only stopped hyperinflation temporarily.

If a long term solution was not found, Germany could slip back into hyperinflation. The short term solution had worked for now but a long term plan needed to be found.

Schacht knew the rentenmark would only ever be temporary given the fictitious nature of its backing and the fact that it could not be used for international commerce – no foreigner would accept rentenmarks.

Schacht knew that only gold backing would be acceptable for the new currency, but Germany didn’t have anywhere near enough.

Restoring the currency could only be done through international borrowing and, after the war, only the United States had the capital.

While attracting foreign capital was not possible when the papiermark had been in freefall, it was possible with the temporary stability created by the rentenmark.

The Dawes Plan

In January 1924 the Dawes Committee began proceedings.

This committee, chaired by American banker Charles Dawes, contained representatives from Britain, France, Italy, Belgium and the USA and was tasked with finding a suitable resolution to Germany’s economic situation with the ultimate aim of restarting reparation payments, which had been suspended.

The Allies, particularly the French, were very interested in currency stability in Germany because it would mean the Germans would be able to start paying them once again.

The Germans, however, needed to find a way to maintain financial and economic stability even when reparations restarted. Schacht was worried that reparations payments would derail the temporary stability the rentenmark had provided.

The Dawes Committee was well aware that reparations could threaten the German currency. So the Dawes Plan created a novel solution whereby reparations funds would be held in escrow by an American Agent-General who would determine what to do with the money and when.

Ahamad explains:

“The plan’s most novel feature was to put in place an ingenious mechanism to ensure that reparations could not undermine the mark as they had in 1922-23. The money to pay reparations was to be raised initially in marks by the German government and paid into a special escrow account in the Reichsbank, where it would fall under the control of an agent-general for reparations who would be responsible for deciding whether these funds could be safely transferred abroad without disrupting the value of the mark. The power was vested in this new office to decide how these funds should be put to use—whether to be paid out abroad, used to buy German goods, or even to provide credit to local businesses. The agent-general would be in a remarkably strong position, a sort of economic proconsul or viceroy. To make his impartiality completely transparent, the committee recommended that he be an American.”

The key feature of the Dawes Plan was a loan of $200 million. The purpose of the loan was three fold:

- Pay the reparations for one year

- Recapitalise the Reichsbank

- Build up the nation’s gold reserves.

In August the Germans accepted the terms of the Dawes Plan. In September the lending began. In October a new currency, the reichsmark went into circulation.

Ahamed:

“In September, the loan that formed the basis of the plan was successfully floated in New York and London. It started a boom in lending to Germany by American banks that was to fuel a recovery in its economy for the next several years and bring stability to the new currency.”

When Was The Reichsmark Introduced?

The new reichsmarks, which replaced the temporary rentenmark, went into circulation on 11 October 1924 with a 40% gold cover.

Rentenmarks could be exchanged at a 1 to 1 ratio with the new reichsmark.

The new mark was tied to gold at the same exchange rate as the prewar goldmark. This meant that a goldmark, a rentenmark and a new reichsmark were all equal.

Therefore the exchange rate between the US Dollar and the new reichsmark stayed at 4.2, as it had been for the rentenmark.

However, despite its gold backing, the new reichsmark was not convertible to gold. Its value came from its convertibility to dollars.

Thus it was really, as Austrian economist Costantino Bresciani-Turroni describes it, a dollar exchange standard.

The rentenmark had succeeded as a temporary measure by giving Germany enough stability to give foreign countries the confidence to provide financial aid. This financial aid allowed Germany to re-establish a currency on a more solid footing with some tie to gold.

However, there was a long term price that still had to be paid.

Fergusson:

“Sanity had returned to Germany’s finances; and no doubt 1924, a period of often extreme monetary stringency, consolidated the financial recovery. But it was too much to hope after the Dawes Plan was adopted in August and unemployment dwindled encouragingly throughout the summer and autumn, that years of reckless profligacy could be so easily paid for, or what the country had passed through would have no lasting effects on the people’s minds. The destitution of the middle classes, of whom the resilient would recover in due course, was only part of the price. The economic reckoning was still to come. Some would say that the political reckoning did not come until 1933, when economic recovery had to begin again.”

Lessons From How Hyperinflation Was Solved In Germany

1. When Government Officials Can’t Get Paid the End is Near

In Ming China, the government’s paper experiment was brought down when the officials no longer wanted to be paid in depreciating currency and demanded silver instead.

In Weimar Germany, some government officials were being paid partly in potatoes while in December 1923 the civil service took a 50% haircut and were promised that they would be paid once the taxes had been collected.

A government can’t operate without a bureaucracy. If the government has no labour because it can’t pay wages, or the currency it offers is not accepted, then the end of the monetary system is near.

2. Government Fiscal Restraint Is Necessary

Monetary reform is necessary to bring hyperinflation to an end. But so is fiscal restraint.

Monetary inflation is like a drug to governments but they need to go cold turkey if they want to give confidence to their currency reform. Confidence will not be inspired if money printing is restrained but budget deficits continue to blow out. If the deficits continue, the temptation to debase the new currency in order to finance them will be too great.

Applying government fiscal restraint will create real hardship when the population has grown accustomed to its largesse. But it is a necessary pill to swallow. The government needs the political fortitude to make it happen.

Weirdly, this is actually easier when the country has hit rock bottom.

As Fergusson describes it:

“The choice had simply become between unemployment and financial chaos or unemployment and monetary discipline. Either alternative meant misery, but the second at least held the promise of food, and a way out of the cul de sac.”

3. A Currency Can Survive With Merely A Perception of Real Value

The rentenmark experiment shows that a currency does not need to actually have real value to survive in the short run. It just needs to have the perception of real value.

The rentenmark was theoretically backed by real assets but it was not convertible into them.

Such confidence tricks can last for a while.

Even the new reichsmark was a confidence trick since it was inconvertible to gold. But that is a more common currency trick that is somewhat acceptable to the public. The rentenmark was something truly novel.

What would have been an interesting experiment (although I would not have wished this suffering on the German people), would have been to continue with the rentenmark just to see how long confidence in it would have been retained.

Currently we are in a five-decade fiat experiment that began in 1971 and we have an inconvertible currency that survives merely on the perception of value. This current system retains its value because the public still has the faith in the creditworthiness of governments.

This lasted a lot longer than many would have thought possible and we don’t know how much longer it will last.

But it too is a confidence trick. We know that its days are numbered and that eventually in the long run we will need to go back to a currency with real value, not just the perception of value.

4. Governments Can and Will Go Around The Central Bank

One of the most interesting parts of the German hyperinflation story is the government’s isolation of Havenstein and the Reichsbank by the creation of the Currency Commission from within the Ministry of Finance.

This arrangement didn’t last long due to Havenstein’s death and it would have been interesting to see how they managed if Havenstein had continued to be President of the Reichsbank for longer.

But it shows that if a politically independent central bank is uncooperative, the government will just go behind their back if it is necessary.

Whether the government’s actions help or hinder the situation remains to be seen.

Schacht’s interventions worked but it was equally possible that the government solution might have compounded the problem and made it worse.

5. A Bailout Is Required

Weimar Germany required a bailout because their gold stock had dwindled to almost nothing.

Luckily for them, the USA was on hand to provide the bailout.

With the current fiat crisis enveloping the whole world, there is no bailout coming.

Jim Rickards, my favourite CIA insider, does a good job of detailing the escalating spiral of bailouts over the last generation.

He notes that Wall Street bailed out Long Term Capital Management in 1998.

Then the central bank bailed out the Wall Street banks in the 2007 – 2008 Global Financial Crisis.

With the central banks now in crisis, Rickards argues there will be no one to provide the bailout in the next crash.

The key difference between Weimar Germany and the present day USA is that the USA still has a lot of gold. So one potential card they could play is to restore gold backing to the dollar at a much higher gold price.

That would, in essence, be the bailout.

6. There is Always a Long Term Price to be Paid

Hard money people like to talk about the death of fiat and the glorious new era we will enter when a hard money standard is finally restored.

That is true and a new hard money standard would be a tremendous boon to real economic growth.

But anyone who thinks there is no long term economic price to be paid for our fiat folly is kidding themselves. The pain won’t end the day we adopt sound money.

Russia has had to pay a heavy price for its 70 years of socialism. Germany had to pay a long term price for its reckless behaviour in the early 1920s. So too we will have to pay the price for the decades of easy money.

We would hope to avoid the political and economic chaos Russia and Germany experienced in those times and I think we will. But at the very least we will have to suffer the opportunity cost of not being on hard money for so long.

It was a temporary German currency introduced in November 1923 to halt hyperinflation

It replaced the Papiermark, which had become nearly worthless due to runaway hyperinflation

It was introduced on 15 November 1923 (following a decree in mid‑October establishing the Rentenbank)

It was created through a reform led by Finance Minister Hans Luther with currency commissioner Hjalmar Schacht administering its issuance from the newly established Rentenbank

No — it was not backed by gold, as Germany lacked sufficient gold reserves at the time

It was backed by mortgages on agricultural land, industry and commerce, with bonds secured against real estate to a total of some 3.2 billion gold‑mark value

By fixing the exchange at 1 Rentenmark = 1 trillion Papiermark and pegging it at RM 4.20 = US$1, combined with a halt to reckless money printing, inflation collapsed within weeks

It restored monetary stability, enabled fiscal discipline, attracted foreign capital (notably under the Dawes Plan), and paved the way for the new gold‑linked Reichsmark in 1924

Yes — it effectively ended hyperinflation, restored public and market confidence, and stabilized the economy long enough to implement a more permanent monetary solution

It was replaced by the Reichsmark on 30 August 1924, which became the new legal tender

The Reichsmark was nominally backed by gold, restoring a gold‑based standard tied to the US dollar peg under the Dawes Plan framework

Conclusion

Germany restored currency stability by abandoning the depreciated currency, the papiermark, and introduced a new parallel currency, the rentenmark.

This new currency might not have worked. The public may not have had any confidence in it and, had that been the case, it would have been a dismal failure.

However, the rentenmark was perceived to be more stable and able to retain its value because it had limited circulation and was backed by mortgages over German real estate.

This provided the temporary stability needed to allow the USA to come to Germany’s aid with a bailout. The bailout allowed Germany to then replace the temporary rentenmark with the more permanent reichsmark, which was pegged to gold although inconvertible.

The bailout allowed Germany to get back on her feet but there was a long term price that still had to be paid.

The cost would start to be counted in 1929.

To your protection and prosperity,

Thomas

P.S. Have I left out anything important? Please let me know. Or if you found this information to be of high value, drop me a line, too. I love hearing from readers.

Sources

Ahamed, Liaquat. Lords of Finance. London: Windmill, 2010.

Bresciani-Turroni, Costantino. The Economics of Inflation: A Study of Currency Depreciation in Post-War Germany 1914 -1923. New York, Ny: Kelley, 1968.

Fergusson, Adam. When Money Dies: The Nightmare of the Weimar Collapse. London: W. Kimber, 1975.

Image Credits

500 Rentenmark is in the public domain

Rudolf von Havenstein is in the public domain

Hans Luther is licensed under CC-BY-SA 3.0

Hjalmar Schacht is licensed under CC-BY-SA 3.0

Bankers and Politicians is in the public domain

Berlin 15 November is licensed under CC-BY-SA 3.0

Charles Dawes is licensed under CC-BY-SA 3.0

Reichsmark is licensed under CC-BY-SA 4.0

{kind=link}

{kind=link}

.jpg){kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}